Can I Get an SBA Loan with No Money Down?:When Lower-Equity Structures Actually Work

Franchable

While the rule of thumb is that SBA lenders often require 10-25% of the project cost to be footed from the borrower ("the equity injection" / "down payment"), the reality is more nuanced. Borrowers often don't realize that any costs they have already incurred for their business prior to applying for an SBA loan can retroactively be counted as part of their down payment. This is especially a handy dynamic when borrowers are applying for a startup loan where down payment requirements usually hover around the 20-25% range and most have already incurred substantial qualifying expenses leading up to the decision to apply for SBA.

Moreover, for business acquisition loans where the borrower is the buyer of a business, deals can be structured with "seller financing". In this case, the borrower gives the seller an IOU, often dubbed a "seller note", which can be treated as debt the borrower owes to the seller post acquisition closing. The seller note can be paid in installments using the cash flows from the acquired business over time. Not only does this help bridge the financing gap if the cash flows support an SBA loan size that doesn't meet the full acquisition price, but any seller note that is put on "full stand-by" even counts as part of the borrower's down payment.

Being put on full-standby means that no portion of the seller note can be paid back until the entirety of the SBA loan is paid back in full. Many sellers will agree to such an arrangement if that's what it takes to get their business sold to an interested buyer utilizing SBA. However, the buyer/borrower cannot rely on a full-standby seller note to take the place of their entire down payment. Most lenders will require at least 5% of the transaction price to come from the buyer's own cash and then accept the remainder of the down payment to be a full-standby seller note.

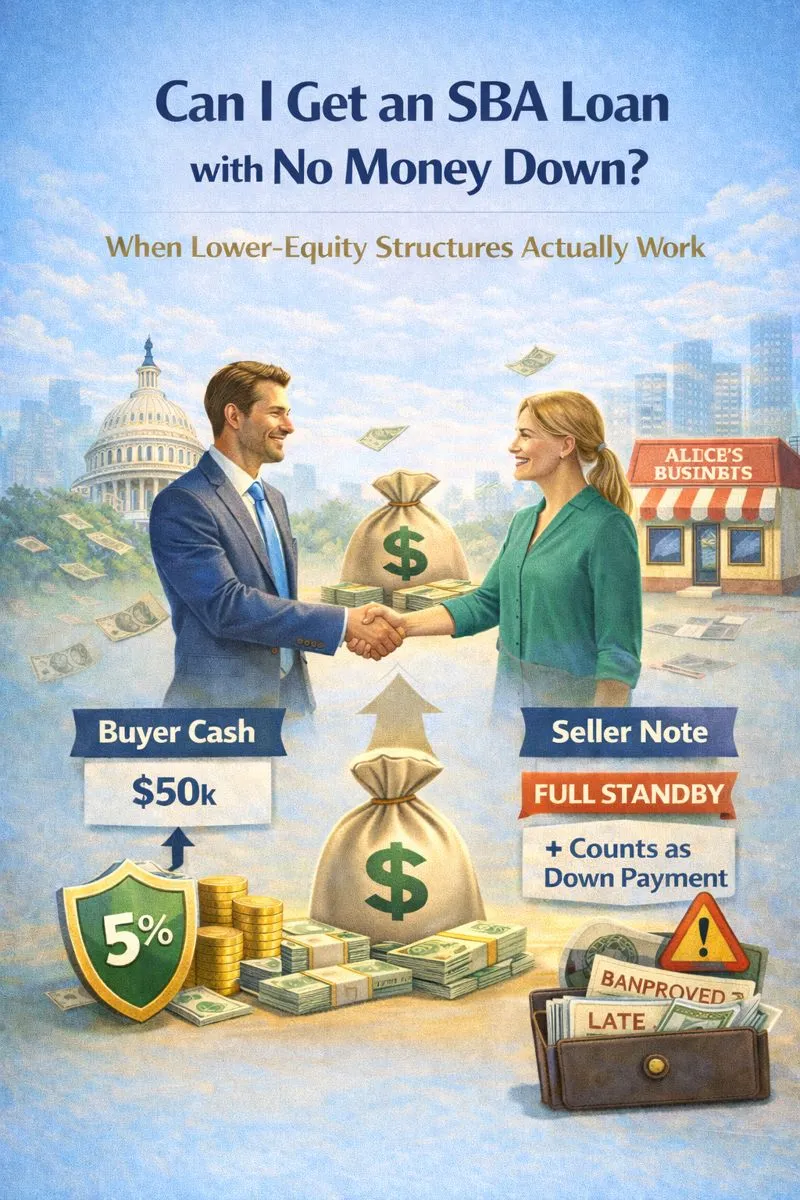

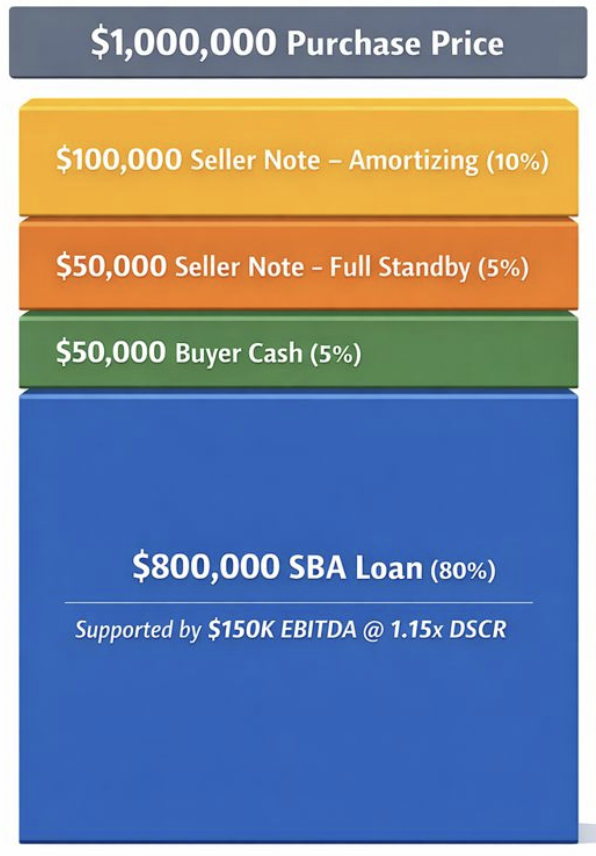

Let us further solidify this concept with an example. Say Bob is looking to buy Alice's business at the agreed upon transaction price of $1M. The business produces $150k of EBITDA so at most, Bob could get a ~$800k SBA loan (1.15x Debt Service Coverage Ratio on $150k EBITDA implies max debt service amount of ~$173k per year which implies $800k loan total at 10-year term and a 10% interest rate). To fund the remaining $200k of the purchase price, the buyer can front $50k of their own cash (5% down payment) and then the seller can agree to structure the remaining $150k as a seller note that the buyer owes to them. $50k of that $150k seller note can be put on full-standby serving as another 5% of buyer down payment (bringing total down payment to 10%) and the remaining $100k of the seller note to be immediately paid in installments following the close of the acquisition.

This is a very common structure employed in business acquisitions that fully complies with SBA requirements while allowing the buyer to minimize their actual cash down payment. Of course, if the seller refuses to subordinate their note to full-standby, lenders will require the borrower to front more cash to meet the 10% down payment hurdle in most cases.

Thus, for borrowers chasing "zero money down", the more productive lever is to see how a transaction can be restructured in cases of acquisition to reduce risk via a seller note, renegotiating valuation, or waiting for the business's cash flow profile to improve. For startup loans, borrowers should be fully transparent on relevant expenditures that have already been made (e.g., legal and consulting fees, deposits, franchise licenses, inventory, equipment) so that they can retroactively count towards down payment.

Platforms like Franchable exist to help borrowers structure lower-equity transactions in a way that reduces risk and increases the likelihood of SBA loan approval. By building lender-grade cash flow models, assessing acquisition fundamentals, and understanding how different SBA lenders treat seller financing and standby debt, Franchable helps ground deals in the reality of SBA bank underwriting.

Explore more articles on SBA loans and franchise financing

View All ResourcesResearch franchise brands

Real FDD data — costs, fees, and earnings — for popular franchises: