How SBA Loans Actually Work:Understanding The Nitty-Gritty

Franchable

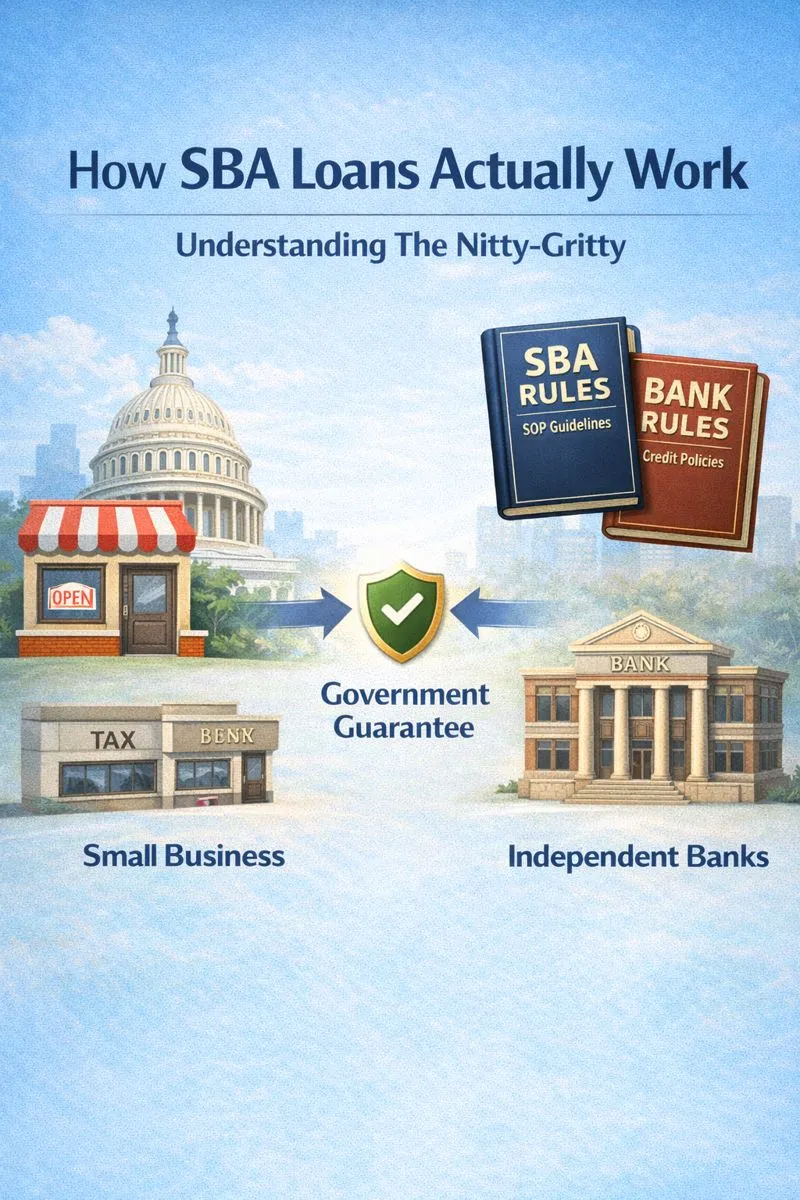

SBA loans are a fantastic feature of the American economy by which private banks can grant long-term credit to entrepreneurs who would otherwise struggle to access conventional loans for the same terms. Many assume that the Small Business Administration under the US federal government is the entity doing the lending but in reality it is independent banks that do the lending – all the SBA agency does is provide a guarantee to cover the majority of the bank's loss should the loan default.

As a result, SBA lenders operate using 2 overlapping rulebooks: 1) the overarching SBA standard operating procedures ("SOP") as set by the agency related to eligibility, structure, and terms; and 2) the lending bank's own internal credit policies set by the bank's credit committee that is taking into account the bank's overall risk exposure across a variety of industries and use cases. An SBA application has to pass both of these filters to get approved.

In practice, when borrowers talk about getting an SBA loan, they are almost always referring to the 7(a) program which is used for starting up new businesses, acquisitions, partner buyouts, working capital, and even purchasing owner-occupied real estate. Under 7(a), the maximum outstanding loan amount (summed across all your outstanding SBA loans) is $5M per borrower at the individual level. If you own more than 50% of a business, you are considered a controlling owner and any SBA loans you personally guarantee for this business count towards this $5M SBA exposure cap. If you own more than 20% but less than 50% of a business seeking an SBA loan, you are still required to personally guarantee the loan with your assets as a co-guarantor but this SBA exposure does not count towards your individual $5M cap because you are not the controlling owner. This distinction is very critical for entrepreneurs tangled in multiple businesses and partnership structures.

Aside: It is important to note that personal guarantees ("PGs") are categorically required from all owners with 20% or more ownership and this is not something that can be negotiated under SBA. This is effectively a contractual commitment by the business owners that they are each personally responsible for repaying the loan if the business itself cannot. This does not mean that the bank expects the business to fail – rather PGs act as a backstop and align incentives to ensure owners remain financially invested in the long-term success of the business.

Most SBA 7(a) loans are structured with a 10-year amortization – meaning they must be repaid in full with the associated interest payments on a 10-year schedule. Prepayments are possible but carry a 3% prepayment penalty in the 1st year post loan closing, 2% the 2nd year, and just 1% in the 3rd year with no penalty thereafter. Now interestingly, 7(a) loans for which >50% of the proceeds are used to primarily purchase or refinance owner-occupied real estate carry a term of 25 years instead of 10 years – in most cases this extended timeline also applies to the portion of the loan proceeds that do not go towards the real estate. This extended amortization dramatically reduces a borrower's monthly burden and raises overall loan feasibility.

The interest rate for SBA loans is generally floating and not fixed – meaning they are based on an index (usually the WSJ Prime Rate) plus an additional 2–3% (this added portion is known as the 'spread' over the Prime rate and is capped by SBA guidelines). The Prime rate itself fluctuates in-line with broader interest rate conditions (e.g., Fed Rate movements) and thus the borrower's interest rate will change over time.

Now from a borrower's perspective, SBA lending can feel quite arbitrary as decisions through conventional routes can take months and feedback is limited. This disconnect is a function of the mismatch between how borrowers think about their business versus how banks think about risk while being constrained by both SBA SOPs and their own internal credit policies. This is why Franchable exists to rectify this gap through extensive experience in understanding why certain SBA loans get denied, preparing all the documents required, helping borrowers get approved despite poor credit, or successfully minimizing down payment requirements.

Explore more articles on SBA loans and franchise financing

View All ResourcesResearch franchise brands

Real FDD data — costs, fees, and earnings — for popular franchises: