What Documents Are Needed for an SBA Loan?:What Banks Are Actually Looking to Learn

Franchable

Borrowers are often surprised to learn how extensive the list of documents required by an SBA Lender can be and even more confused on why certain documents are required at all. Weeks of uploading files, answering follow-up questions, and revising submissions can take their toll on applicants, with the borrower left wondering how their documentation is actually used in the bank's decision-making. Our goal is to break down this black box and help borrowers understand how each request helps lenders evaluate risk and borrower capacity to repay.

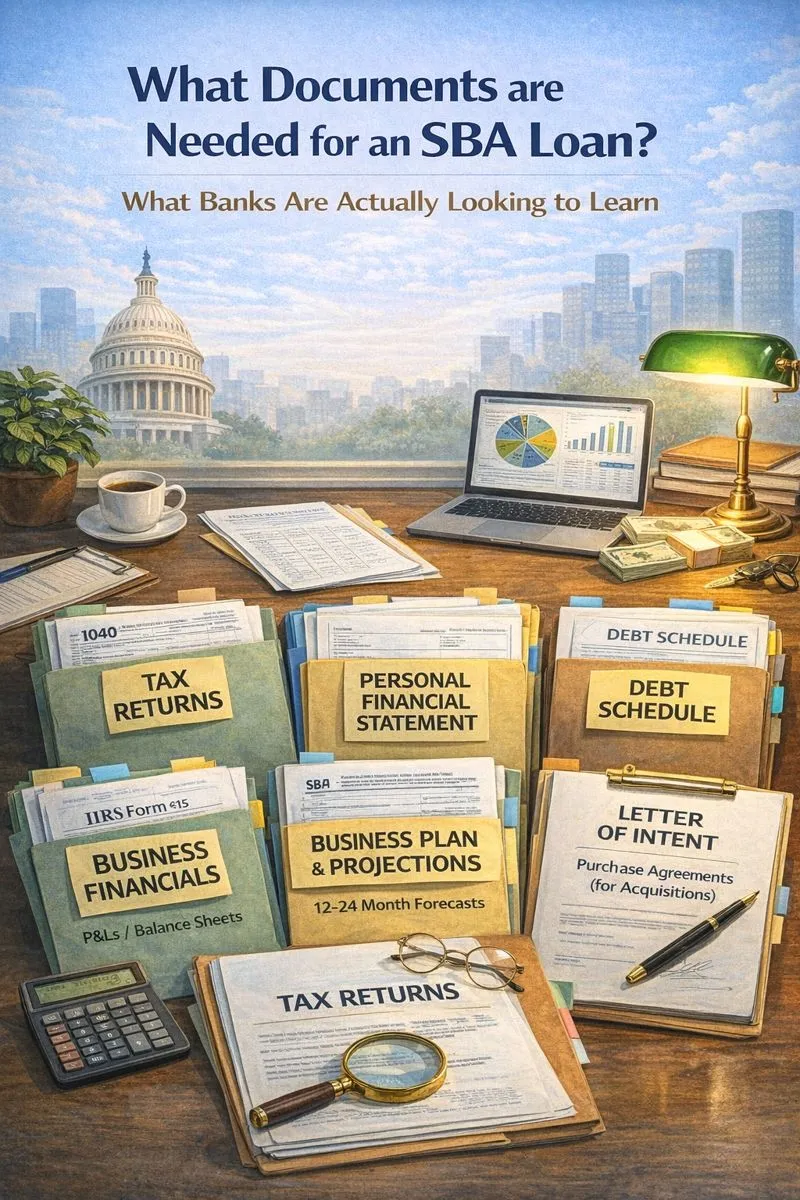

Lenders start by assessing the personal financial position of the borrower and any co-guarantors (any individual who owns more than 20% of the borrowing entity). This involves every guarantor filling out and submitting an SBA Form 413 (also known as the Personal Financial Statement or "PFS") where you self-report and list out major personal assets and liabilities (not ones held by any business entity). Additionally, every guarantor provides personal tax returns for the most recent 3 years. Together, this information helps lenders evaluate the borrower's ability to absorb financial stress and make debt payments if business performance is lackluster.

When filling out the PFS, the most important thing is coherence rather than perfection (less about accounting everything down to the dollar and cent). Any major inconsistencies that do crop up between the tax returns and stated assets or liabilities will slow down the process.

If your existing business is seeking an SBA loan for expansion or refinancing (not relevant for startup loans), you will be required to provide 2–3 years of annual P&Ls, a latest monthly balance sheet, an up-to-date debt schedule, and business tax returns. This enables the lender to assess whether the business generates sufficient and consistent cash flow to service the requested debt amount. Lenders are typically looking for EBITDA to be at least 1.15x–1.25x the annual debt service amount, inclusive of interest and principal repayments.

Any major volatility, margin swings, or prolonged unprofitability will be viewed as red flags and require additional explanation. Businesses over 1 year old will often need to be EBITDA positive, while those less than 1 year old must show a clear trend toward impending profitability. One of the most common sources of delays is material discrepancies between historical P&Ls and business tax returns — these must be reconciled with clear explanations.

For startup loans, lenders require financial projections for 12–24 months, including forecasted P&Ls, balance sheets, and cash flow statements. Banks are less concerned with precision than with reasonableness. For franchise startups, lenders will often anchor to Item 19 disclosures in the brand's Franchise Disclosure Document (FDD) as a reference check for revenue and margin assumptions. Some lenders also require a business plan that summarizes the market opportunity, competitive landscape, and risk mitigants. Physical brick-and-mortar businesses will ultimately need to provide the executed lease as well.

SBA loans for business acquisitions require a Letter of Intent (LOI) outlining the transaction structure, along with supporting documentation such as seller financing agreements. Transactions involving real estate require additional materials including appraisals, while partner buyouts necessitate detailed cap table disclosures.

While the process can feel taxing, document submission is less a clerical exercise and more about creating an underwriting narrative. Lenders need to build comfort around debt service capacity and downside risk. Borrowers who understand this and provide documentation through that lens tend to move faster, receive clearer feedback, and avoid unnecessary dead ends.

Franchable helps borrowers streamline this process through its SBA lending platform by providing templates, document checklists, and mediated communication between borrowers and lenders, while also delivering lender-grade projections and business plan support. The ultimate goal is to ensure documentation aligns with how banks actually underwrite, making the process faster, clearer, and far less frustrating.

Explore more articles on SBA loans and franchise financing

View All ResourcesResearch franchise brands

Real FDD data — costs, fees, and earnings — for popular franchises: